Artwork - Black Pearl by Melbourne based Theo Papathomas

(We love Independents here at Resolve, and think that artwork can stimulate thinking which some articles cannot. So from now on, we will be promoting local art talent)

Paper Executive Summary:

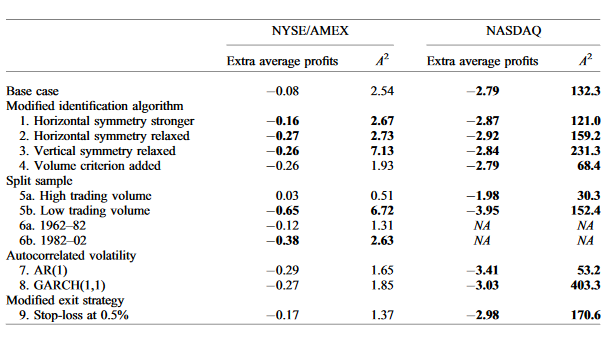

Head and Shoulders Trading pattern strategy doesn’t work in US equity markets, both the NYSE and AMEX stock exchanges, from 1962 - 2002. Analysis found that there-was an unusual trading volume, which could not be attributed to ‘auto-correlation volumes, price volatility or stale limit orders.’ “Statistically significant excess trading takes place on four or more trading days around the neckline-crossing and totals 60% or more of a day’s volume. The paper does note that currency markets are different to the stock exchanges studied in this paper, citing that 90% of currency traders in London and Hong Kong, Singapore & Japan (Lui and Mole, 1998) rely on technical analysis. However, it is important to make distinct that this is a measure of number of traders, and not total capital volume in the markets. ‘Studies of currency markets find that most technical strategies are profitable both before and after adjusting for transaction costs and risks (Menkhoff and Taylor,2007)

No other fundamental economic or business-related signals were used to determine entries. Trades were exited automatically if a loss of 1% or more was incurred. Theory also suggests that noise trading is beneficial. It can provide camouflage [and much needed liquidity] for informed traders; it can help exchanges achieve economics of scale and lower costs for all traders and can help markets avoid no-trade equilibria. Uninformed noise trading brings higher overall trading volume and lower spreads.

Reflections:

Humans are programmed to find patterns automatically. People will find illusory correlations between randomly matches pairs of words and between randomly matched psychological symptoms and patient drawings. (Chapman & Chapman, 1976) psychologists have shown that social forces are especially powerful when there is little objective information. (Sherif, 1937,cited in Shiller 1989) We are information organising machines, desperately trying to justify or existence and worldly bias's. Combine this with the lust and allure to make money, you will find all sorts of rationale for what can happen, and perhaps worse, what has happened.

There is a delicate balance between confidence, fooled by randomness, time, experience and knowledge. Acquiring knowledge takes time and applied knowledge is experience. However, you gain firsthand experience without application of the knowledge, which will mean, in points in time you will have to behave ‘irrationally.’ How can anybody behave rationally, if, you are not-certain of the outcome? The definition of rational is to behave with reason and logic. However, as stated above, to be reasonable is to be somewhat certain of the consequences of the choices which are in front of you. If the consequences of the choices are somewhat unknown, then how can an agent be expected to behave rationally?

Therefore, there is a delicate balance between these concepts.You need to be in a constant state of learning, (knowledge) to be able to apply those leanings (experience) with any sort of confidence. Yet you cannot actually be sure that the knowledge is true, in the sense that it will produce the outcome which is expected. So you have to initially apply the knowledge without the experience (and maybe the confidence depending on the subject.) Once the content of the learning has been applied, experience is gained, and further learning's are applied.

Understanding the learning process, and sticking to a firm process is critical to the success of any trader in this environment. But more importantly, self reflection and a constant learning mindset, while humble enough to acknowledge randomness is most appropriate.